Economic News: May 2026 Pulse Check On Florida’s Economy

May 2026 Pulse Check On Florida's Economy

In a time of national economic uncertainty, Florida’s economy continues to play on a global scale. If Florida were a country, it would be the 15th-largest economy in the world, with our GDP at approximately $1.8 trillion. The size of Florida’s economy is measured through GDP, a metric that has only gone up over the last few years – and is expected to continue to. But it isn’t the only metric that measures the health of an economy. Many other statistics provide additional insight into the economic reality that Floridians are experiencing every day, and those metrics are seeing a lot of movement right now.

Headlines, like a recent Wall Street Journal article, “Florida’s population boom fizzles as high costs drive away middle class,” are pointing to slowing population growth, higher costs, and an uncertain labor market. We’ve looked at all the economic indicators at play, and below is a snapshot of the key trends currently shaping Florida’s demographic and economic shifts:

Florida’s Migration is Slowing

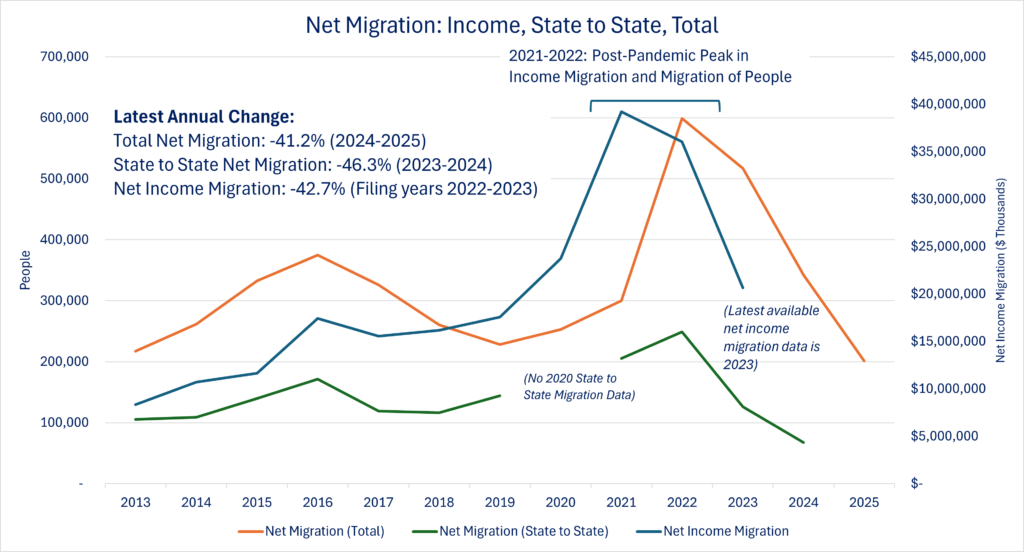

- Florida’s net migration of people from other states totaled 67,630 in 2024 (latest available data); a 46% decline from the prior year, and the first time domestic net migration has been under 100,000 since 2011.

- Total net migration, including international migration, to Florida reached 201,191, down 41% (nearly 140,900) year over year (2024-2025).

- Florida welcomed a net of 551 new residents every day in 2025; Domestically, that is a net of 62 people moving to Florida every day, and internationally a net of 490 people.

- Migration of people is slowing across Florida, with only nine of sixty-seven counties experiencing faster net migration than the year prior: Calhoun, Charlotte, Madison, Okaloosa, Sarasota, St. Johns, Sumter, Union, and Wakulla.

Florida's Income Migration is Top in the Nation, but Seeing Declines

- Florida remains a top state for attracting income and investment, driven in part by its competitive tax climate and favorable policy environment, thanks to the Florida Business Agenda, EOG and policy leaders in the legislature, and many of you.

- The average adjusted gross income of new Florida taxpayers exceeds $122,500, higher than any other state. In fact, 5 of America’s 6 wealthiest residents now reside in Florida.

- Income flowing into Florida is a vote of confidence in our state’s economy, but it also can fuel rising prices, leading to affordability problems. Once a low-cost state, costs like housing have been driven up, in part, by a rapid inflow of high-income households and many areas of Florida now have a housing affordability challenge.

- The latest data available shows that in 2023 Florida was #1 in the country for net income migration. However, this indicator is also on the decline. Net income migration from other states declined by 43% from filing year 2022 to filing year 2023.

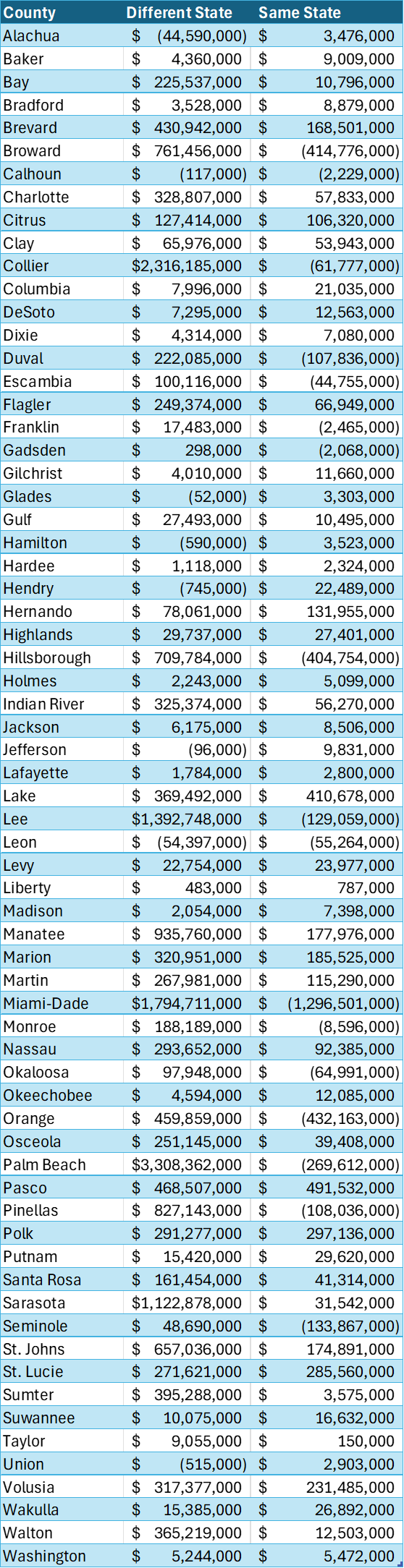

- Almost all counties in Florida attracted this income from other states, with Palm Beach ($3.3B), Collier ($2.3B), and Miami-Dade ($1.8B) gaining the most net inbound income over the year. Many counties in Florida are seeing net income migration levels that rival or exceed those of entire states, with Florida’s top 5 counties individually performing at income migration levels that would rank them among the top 10 states nationwide if they were measured as states. For example, Palm Beach County had $550 million more federally taxable personal income move in than #5, Arizona.

- There are also emerging intrastate migration and income redistribution trends within Florida. While large metro areas in South and Central Florida see the most net income migration from outside of the state, cohorts of already established Floridians are moving to counties outside of these metro areas. Palm Beach, Miami-Dade, and Lee County are among the top for attracting out-of-state income but are seeing the most income move to other Florida counties.

- Not all counties have seen high-income migration, with eight losing net income to other states. Leon County (-$54M) and Alachua County (-$45M) had the largest net losses in income to other states. Leon County also had a net loss to other counties.

Florida's Labor Market Cools Alongside the Nation's

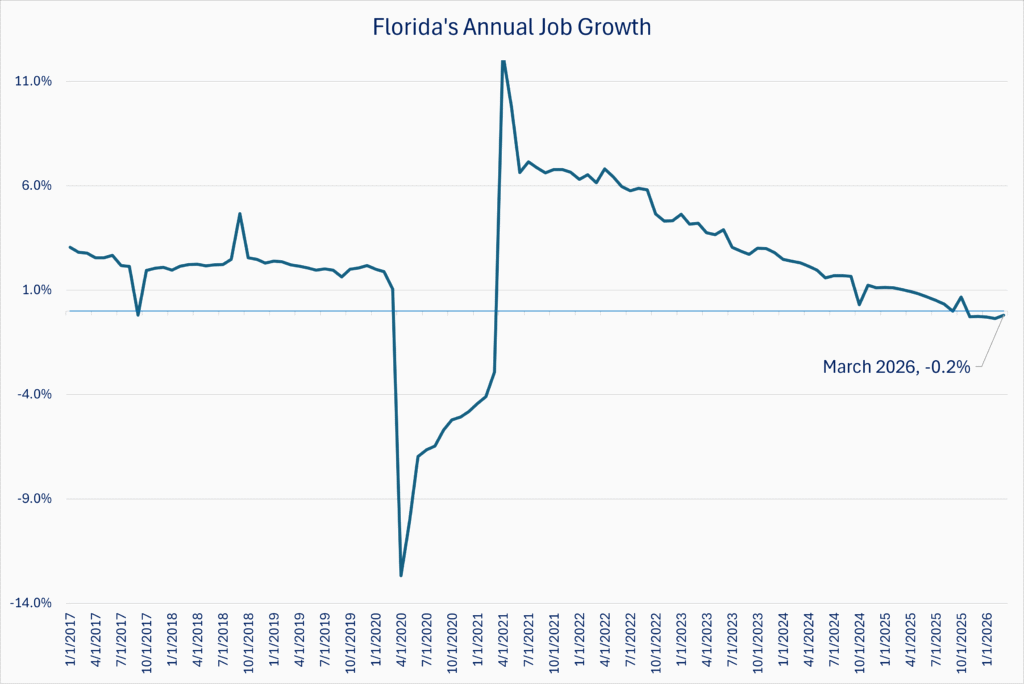

- Florida’s labor market has been cooling since late 2025.

- Florida lost jobs in 2025 and lost 22,400 jobs over the year (March 2025-March 2026), a loss of 0.2 percent.

- While the national labor market is also seeing a cooling, the U.S. did see annual job gains in March 2026 (+0.2 percent).

- Florida has lost jobs annually every month since November 2025. Prior to these five consecutive months of job losses, there had not been multiple months of job losses since the pandemic (April 2020 to March 2021).

- Florida’s unemployment rate is 4.7%, up 1.1% from a year ago. This is the highest it has been since July 2021. The national unemployment rate is 4.3%. The number of people who can’t find jobs in Florida is now over 500,000. The number of Florida jobs that can’t find people totals 452,827.

- Rising unemployment is the reality across every county, with Sumter County (7.8%) seeing an increase of 2.2 percentage points in its unemployment rate over the year, and the lowest in Miami-Dade (2.9%), an increase of 0.2 percentage points. Taylor County has the highest unemployment rate in Florida (8.4%), while Miami-Dade County has the lowest (2.9%).

- Younger workers are disproportionately impacted, with unemployment among ages 16–24 at 11.0%, compared to 3.4% for prime-age workers (a gap of 8 percentage points between the two age groups).

- The U.S. gap is smaller, with only a 6.1 percentage point difference between young workers and prime age workers.

- The largest contributor to unemployment is Floridians who are struggling to enter or reenter the workforce (rather than Floridians losing their jobs). This characteristic of a “low hire, low fire” labor market means businesses are not laying off employees but are slow to hire in the face of economic uncertainty.

- The biggest driver of unemployment in Florida right now is young workers entering the labor market and being unemployed for longer. In February, Floridians seeking work were unemployed for an average of 25 weeks, compared to 21 weeks a year ago.

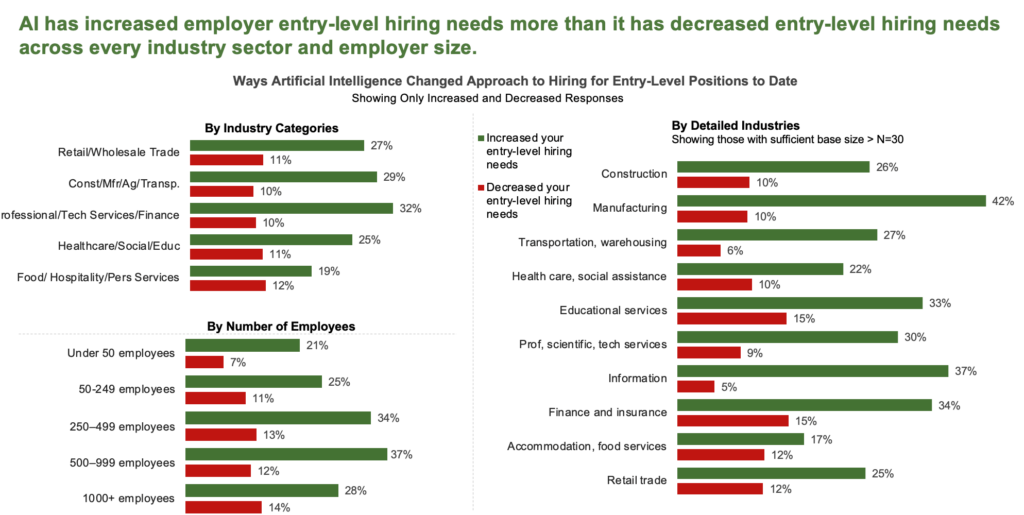

- In the face of a shifting labor market, the common question is the impact of AI. The reality is that no one can put a number on it. Innovation is happening every day, which is shifting the job market – but currently, early signs point to less of an impact than people may expect and some say AI is creating new jobs that didn’t exist previously. Businesses are slow to hire in today’s job market, and a portion of that could be AI. But there aren’t widespread layoffs due to AI. Economic uncertainty and automation are playing a much bigger role in these labor market dynamics than AI is. Time will tell, but for now, jobs are being reshaped, not eliminated. Artificial intelligence is not the chief engine of the declining job market.

- In fact, across industries and employer size, AI has actually primarily increased entry-level hiring needs.

Replacing Childhood Poverty with Self-Sufficiency is Not a Social Program—it is Economic Development

- Florida is experiencing two different phenomena: high net income is moving into the state (albeit at a slowing rate), seeing Florida as the best place to work, retire, and invest. However, the reality is different for a large portion of the population.

- 34% of Florida’s households are ALICE (Asset Limited, Income Constrained, Employed), meaning they make income above the federal poverty line but below the household income needed to afford essential costs in Florida. These households must decide between payments such as rent, food, childcare, auto, and utilities.

- Shining a spotlight on ALICE households and households who are living below the federal poverty line (which, combined, is 47%) shows that our Florida Prosperity Initiative is not a social program – it is an ambitious form of economic development, as many of these Floridians are also our core talent base.

- While Florida has more children, childhood poverty has declined by approximately 3,200 children. The Florida Chamber Foundation’s Florida Prosperity Initiative reports there are 711,576 children in poverty, and over half of these kids in poverty live in just 15% (152) of Florida’s 983 zip codes. Incredibly, Miami-Dade County has more children in poverty than 42 of Florida’s 67 counties combined. Philanthropy is aligning around these zip codes and the Florida model. It’s another economic development effort that shows promise.

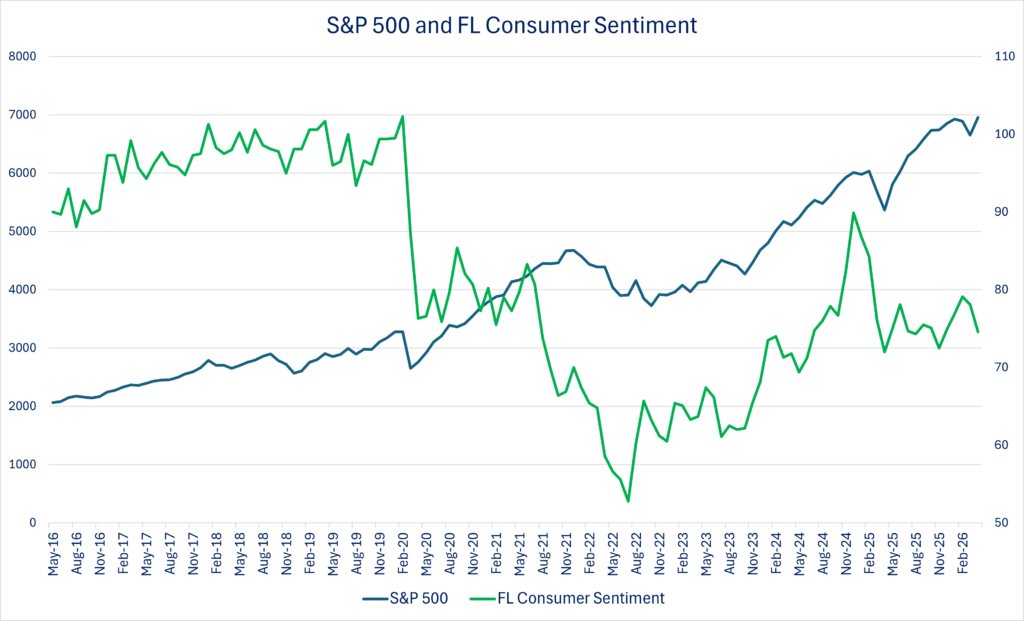

Assets and Consumer Sentiment Trend in Different Directions

- Assets and consumer sentiment are trending in different directions, meaning that increasing economic value for some does not necessarily mean perceived improved financial circumstances for all. Additionally, not only are these trending in different directions, but the U.S. stock market is seeing close to all-time highs in the same period where our nation’s consumer sentiment is seeing an all-time low. Florida’s consumer sentiment is following a similar trend. While economists know the stock market is not a proxy for the economy, it’s important that Florida’s leaders pay very close attention to middle Floridians, skilled trades, and reducing costs.

Florida's Industries At a Glance

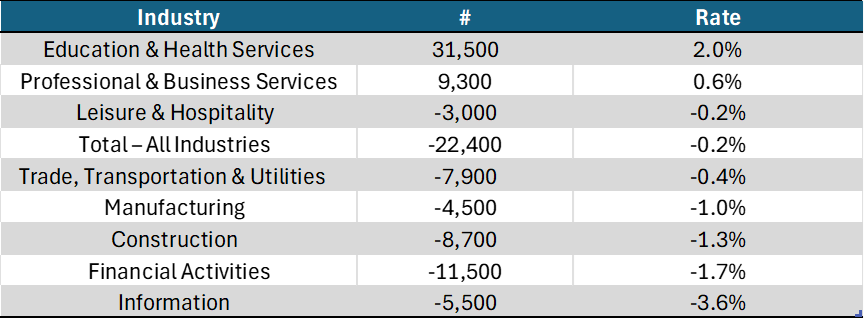

While we remain bullish on Florida’s targeted industry strategy, especially as local economic and community development efforts align local workforce and diversification strategies, not every industry is adding jobs. Here is a recent snapshot by industry:

Florida Names 12 Target Industries to Diversify the Economy

As we work closely with FloridaCommerce, Select Florida, and many others, it’s important to acknowledge that Florida’s growth and diversification strategy officially names 12 target industries to attract and grow in our state. While many residents know of Florida’s important tourism, agriculture, and construction industries, most Floridians aren’t aware that central Florida is the global epicenter of modeling and simulation ($8B) or that Florida is ranked #11 for manufacturing jobs (and is the fastest growing). Here are Florida’s official target industries:

- Logistics

- Manufacturing

- Research and Development

- Aerospace and Aviation

- AgTech

- Energy Security

- Financial Services

- Information Technology

- Life Sciences

- Maritime

- Military and Defense

- Corporate Headquarters

Bottom Line:

As our President & CEO Mark Wilson often says, “If Florida was a stock, I’d be investing in it.” Florida must focus on the fundamentals of free enterprise and not rely solely on attracting wealth and capital expenditure at a time when middle market talent, and families move out of high-cost areas to other counties or states. The numbers are the numbers, and championing free enterprise is always the right answer. Even as these numbers shift and trends change course.

The Florida 2030 Blueprint invites alignment between workforce and economic development plans that position Florida to further grow and diversify our economy.

The Florida 2030 Blueprint was a guiding light before the unprecedented growth post-pandemic (2022), it was a guiding light through that expansion, and after it was updated in early 2026 via the Florida 2030 Blueprint Halftime Report, it will continue to be as Florida weathers a shifting demographic and economic landscape, unifying Florida’s business, policy, and nonprofit leaders.

To stay up to date with the latest on Florida’s economy, subscribe to our monthly Florida By The Numbers updates.

Join us for the 2026 Future of Florida Forum, Florida’s premier annual business leaders gathering, where we’ll dive deeper into Florida’s business and economic landscape. Click below to learn more.